Download The 2025 M&A Report For Free!

Your download is on the way to your email inbox!

Please make sure your email is typed corectly.

All information is protected & secure.

Private equity doesn’t always “work.” Hopefully, this comes as no surprise. Private equity’s involvement in the car wash sector is no exception. The formula that combines outside money, tenured industry experts, and a fitting and applicable industry is far from infallible.

Private equity doesn’t always “work.” Hopefully, this comes as no surprise. Private equity’s involvement in the car wash sector is no exception. The formula that combines outside money, tenured industry experts, and a fitting and applicable industry is far from infallible.

The first half of 2024 has brought a major and significant slowdown in carwash M&A, along with a stark decrease in the dispersion of acquiring parties. Transaction count is down ~46% and the number of sites sold and acquired is down nearly 40%, both compared to the first half of 2023. By way of most active acquirers, 2024 posted a large increase in deal concentration. Most notably, during the first half of 2023, the most active acquiror by transaction count was El Car Wash, having been the acquiring group in just 11% of the announced transactions. The first half of 2024 had Whistle Express representing a commanding 43% of deals as the acquiring group. In this industry report, we cover all announced M&A transactions in Q2 and provide a candid overview of market trends.

CWA News Exclusive

With the increase in private equity and outside investor activity in the space today, it’s important to realize that this is not the first time. Outside investors have historically poured into this industry with a promising glimmer and hope to consolidate a fragmented world with high margins.

The history of private equity in the industry is long, involved, and nuanced. The historical depth makes covering this topic in a concise format difficult. For this reason, this article takes a narrower approach by discussing just one singular company and its journey and evolution over time: International Car Wash Group – aka “ICWG.”

ICWG is a particularly illustrative and interesting subject under the current lens of focus. Not only is it the largest single car wash operator in the world, but it has a deep and rich history of being owned by a full roster of different private equity investors throughout its existence. ICWG and the Company’s history exemplify many of the key tenants and trends of private equity’s involvement in the sector, which makes it an ideal showcase example.

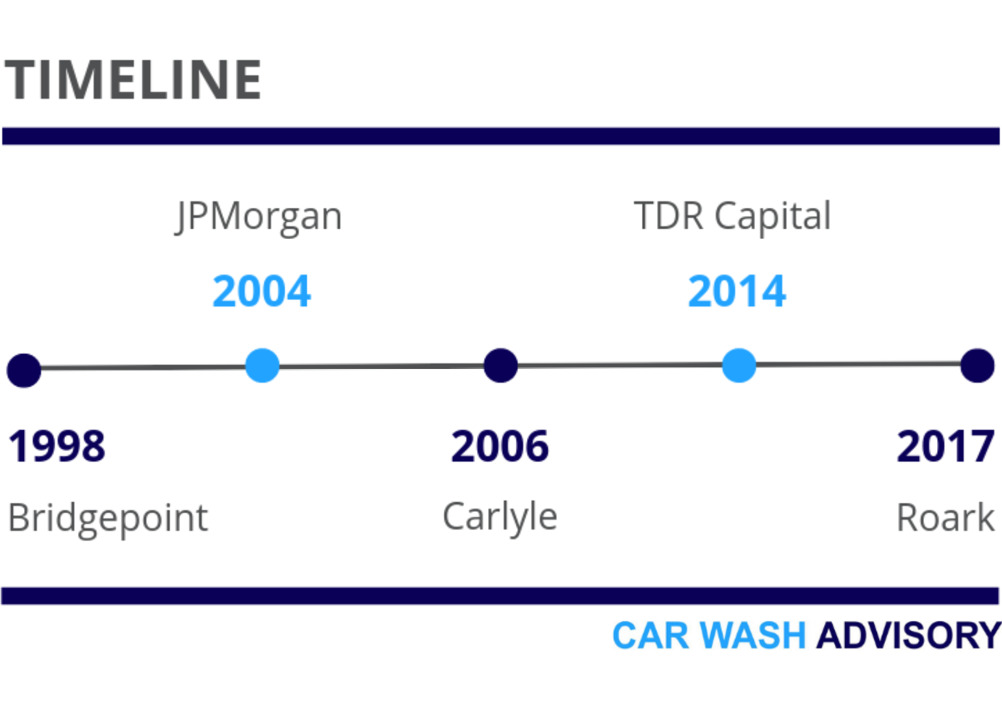

ICWG was founded in 1965 in Germany under the name IMO. The company still operates under the name IMO in non-US locations. Bluebrook and ARC also exist in the company’s history. Despite the many names, it is the same company, and for simplicity, IMO / ARC / ICWG and Bluebrook will be referred to as ICWG for the rest of this piece. Furthermore, this exploration will focus on ICWG’s history after Bridgepoint Capital became involved in 1998.

.jpeg)

Before delving further, it’s important to lay out the nuances unique to ICWG as a company. All companies are unique and different from their competitors in some ways. These differences do not always make the analogous extrapolations and ability for peer comparison null and void. However, one should be aware of and consider them when drawing insights from such exercises.

Firstly, ICWG is an international corporation. With different towns in the same state having different demographic and consumer patterns in the car wash industry, one can only imagine the extent to which this is true across different continents. Along with being international comes both good and bad. A company can mitigate certain geographically specific risks. However, this exposes a company to new challenges in management, consistency, and scalability, among many others. It is fair to say that this international footprint and history does not mean ICWG is incomparable to domestic endeavors, but it does introduce some inherent differences.

Also relatively unique to ICWG is its transformational mega-acquisition past. Essentially, ICWG experienced one single acquisitive transaction that grew the company to an extent unrivaled by all other acquisitions in the company’s history. Oftentimes, an acquisitive growth strategy manifests itself through many serial small-to-medium-sized acquisitions, especially in a fragmented industry. Although ICWG certainly did, and still does, partake in said strategy to some extent, the single acquisition of Toman Group in 2002 skyrocketed the ICWG business's size to the +800 wash number.

Bridgepoint Capital became involved with ICWG in 1998 with a clear objective and strategy: growth through acquisition. Armed with an executive team largely consisting of ex-oil industry execs, including Bret Holden at the helm, the strategy was set. Bridgepoint paid ~£115mm for ICWG and wasted no time starting their shopping spree. This is evidenced by their massive 2002 acquisition of the former sister German company Toman (which was actually spun out in 1990 to free capital for UK expansion) and many others. Overall, during the roughly five years that Bridgepoint Capital owned ICWG, it doubled the company’s size in the number of washes. It is fair to say that Bridgepoint Capital’s ownership of ICWG was a success. The company disclosed that during this time, the number of ICWG washes doubled, and EBITDA tripled.

JPMorgan Partners entered the ring in 2004 when it purchased the now behemoth ICWG from Bridgepoint for £350mm. JPMorgan Partners, the internal private equity arm of JPMorgan at the time, did not continue with growth at the same pace as its predecessor. JPMorgan kept Bret Holden as CEO when they bought the Company. However, they came in with the mission of focusing on the operational side to provide a better-in-class offering even further than ever. This is not to say they halted acquisitions and new development growth but simply slowed it down. JPM wanted to increase the market share of pre-existing washes under the Company’s umbrella.

JPMorgan held ICWG for roughly two years and made what can be presumed as a favorable exit by selling it in 2006 for £450mm. This is undoubtedly one of those times where not having full financial performance and the details of purchase price consideration and structure only provide a partial picture. Conclusions as to investor return should be drawn cautiously.

The most tumultuous and interesting portion of ICWG’s history is undoubtedly its time with Carlyle.

Carlyle purchased ICWG from JPMorgan Partners in 2006 for a total price of £ 450mm. Carlyle entered this investment to achieve incremental growth on top of what the established and record-setting juggernaut had already achieved. Carlyles’ initial press release cited Andrew Burgess, a Managing Director of the Carlyle Group, stating, “…we believe there are significant further growth opportunities across Europe.” In that same acquisition announcement, Bret Holden noted, “We believe Carlyle will be well positioned to help IMO ramp up growth and further expand the business geographically.”

Carlyle’s investment in ICWG was a complete failure, plain and simple. Carlyle lost everything. Not only ICWG's nine-figure initial equity investment, but also the money it further injected into the company in 2008 in the form of mezzanine PIK debt to stem the bleeding led to the failure. Carlyle was forced out in a landmark restructuring case in which mezzanine lender rights and valuation approaches were pushed to unprecedented attention. Without going into the details of the now legendary case, let it suffice to say that Carlyle and the junior creditors did not win in the restructuring process. Ultimately, control of the company lay in the hands of the consortium of senior lenders.

From a high level, the cause of this restructuring was the company reaching a point of no longer being able to comfortably and confidently service its debt obligations. This presented itself in the way of the company breaking financial covenants with creditors. Carlyle even tried to convince creditors to allow the company to do sale-leaseback transactions with owned washes and properties to provide an immediate influx of cash flow to keep the company afloat (a practice that is now relatively commonplace in the industry today). Overall, Carlyle stated it was a combination of global economic conditions and two years of unfavorable weather.

To avoid opining about true causation and to provide unbiased objectivity, let us delve into the takeaways that can be gleaned from purely factual and public data.

A common misconception often propagated and reinforced is a false definition of what it means for an industry or business to be "defensive." Without getting into the nuanced differences between a lower correlation coefficient and a negative one, a defensive business is more often than not impacted less than the overarching economy. It does not mean that it is not impacted at all. It also does not mean that in a down economy, the subject actually does better on an absolute basis. It rather means that it has a numbed downside elasticity under said circumstances.

Many often refer to car washes, especially the lower ticket price express model, as being very "defensive." It is true to some extent but is often misconstrued. With the recent and continued advent of the lower ticket price model, it is worth bringing this up. Even if more people doing higher price (let's say full-service type) washes move down to lower price tier express washes, the denominator, or overall population, still shrinks. So, although the ratio of numerator to denominator of these lower ticket price relative market shares increases, the absolute value and top line decreases.

Capital structure and debt loads are not always the cause of a business's problems, even when aggressive and highly leveraged ones are used. Sometimes, capital structure isn't the actual impetus of a problem, but rather the inhibitor of finding a solution to a problem. And sometimes, capital structure has nothing to do with a problem.

Being a point of highest contention in relation to Carlyle and ICWG's situation, the facts must at least be addressed here. Without delving into a debate about what financial prudence means regarding forming a capital structure and without the hardest of figures, let us just discuss what we do know.

Carlyle leveraged the business. Carlyle originally bought the company with a mix of both debt and equity for a total purchase price of £450mm in 2006. At the time of the 2009 restructuring, there was £403mm of total debt (£313mm being senior debt). Courts agreed that the company was simply not worth anything over the fulcrum point that would allow for junior creditors to hold any residual claim of substance, or in other words, they agreed and ruled that the PWC prepared valuation analysis that ascribed a total company valuation of £ 265 max was realistic and accurate, therefore assigning zero value and rights to all junior creditors and equity holders. Published financials from the first half of 2018 showed that the company had prorated leverage of ~8-9x.

Carlyle Paid More per Wash Than JPMorgan Partners Carlyle purchased the business for a significantly higher price without many more washes than the prior buyer. Carlyle specifically paid ~30% more (in total purchase price consideration) than the sellers from which they bought it had paid just two years prior. The wash at the time of Carlyle's purchase had only ~7% more washes than that of when the prior buyer and current selling counterparty, JPMorgan Partners, purchased it in 2004. We do not have the entire picture here. Without comprehensive profitability figures, it is unfair to insinuate that Carlyle definitively "overpaid," let alone that they even paid a higher true cash flow-based multiple.

This is undoubtedly the most ambiguous of the takeaways, but it is not to be undervalued. With private equity hands back in the mix, this is an excellent example of how the same company, albeit with different macro market conditions, does not result in the same investment performance. This is even more true for highly operator-discretionary businesses such as car washes. Though a simple and intuitive point, it often seems to be forgotten, and this is demonstrated through a piggyback “me-too” tendency that appears to unshakably lurk behind private equity, following them into many industries in which it becomes heavily entrenched.

After much turmoil, after a drawn-out sales process in which a 2012 bid was rejected only to come back in a different form and accepted years later, TDR Capital finally bought ICWG in 2014. The exact terms of TDR’s purchase were never disclosed; however, it was openly rumored and speculated that TDR Capital paid around£250mm for the company. If the widely accepted rumors are true, the restructuring judgment back in 2009 was spot on in its valuation conclusion. TDR Capital had openly been looking at ICWG since 2008 and was well up to speed on the company by the time their offer was finally accepted.

TDR Capital hit the ground running with a clear and openly stated mission – use the current cash cow to focus on disciplined accretive acquisitions in the U.S. market. TDR did precisely that during their time with ICWG. Under TDR Capital, ICWG entered the U.S. market, and by the time TDR was to exit their investment, they would have a presence of over 110 car washes in the U.S. Under TDR, ICWG did more than just the U.S. entrance. The company also invested significant capital and effort into a refurbishment program, Australia Development, and evening-established plans for opening washes in China.

Roark Capital is the current owner of ICWG and purchased the company in 2017. Roark Capital has made their aspirations involving the company completely public, concrete, and crystal clear; to grow ICWG to be the leader in the U.S. market. Roark is certainly well on their way, already having over 150 washes in the U.S. (the company’s most recent acquisition of two Wash N’ Roll sites just this past May of 2019). The order is tall, and ICWG has their work cut out for them as they currently sit at just half the size of Mister in the U.S.

In 2020, International Car Wash Group (ICWG) was acquired by Driven Brands, a diversified automotive company with offerings ranging from oil changes through its Take-5 brand, automotive glass replacement via Auto Glass Now!, to paint and collision services through Maaco and Meineke. Driven Brands went public in January 2021 with a market capitalization of approximately $3.4 billion, leveraging the IPO to fuel its aggressive growth strategy, which has included expanding its footprint in the car wash industry.

Private equity is in the sector and shows no signs of slowing down its involvement. This is not the first time this has happened. Although we only delved into the history of one specific wash company today, I assure you there are many others (some still around today and some no longer in existence) with deep and interesting histories of financial sponsor involvement.

Despite often being viewed as simple through outside eyes, the car wash business is extremely operator-discretionary and is not a naive, pure plug-and-play model. Sure, it is most certainly not rocket science. But rocket science isn’t as competitive of an industry, and they don’t often have to worry about part-time employee turnover.

The industry is undeniably attractive for private equity and external investors, and rightfully so. It’s a wonderful fertile land for growth, operational efficiency improvement, rollup synergies, and stable high-margin cash flows. That said, it does not mean that being successful is as easy as paying enough to build an empire. As with all investment strategies, judicial approaches and financial prudence are crucial. A rising tide lifts all ships, and the lack of the aforementioned strategies and tenants can be absent while still experiencing success in said waters, it is when the tides shift that they become mandatory to survive and weather the storm.

As has happened before and will happen again, there will be winners and losers, not only company by company but investor by investor as well.

With private equity’s growing interest in the car wash sector, the industry’s appeal lies in its potential for stable, high-margin cash flows and growth through strategic consolidation. However, the car wash business is far from a simple plug-and-play model; it requires sharp operational insight and careful management to succeed in a competitive landscape. Investing in car washes demands not just capital but a disciplined, judicious approach to maximize returns and sustain growth.

Car Wash Advisory is an M&A firm solely dedicated to serving the car wash industry. Contact us to learn more about our car wash M&A firm.

.png)

Is Mister Car Wash a take-private candidate? Explore valuation compression, private vs. public market dynamics, and lessons from Dentalcorp’s public-to-private journey.

Our Top Companies and Top Acquisitions pages have become trusted resources across the car wash industry. We’re inviting the community to help keep these tools accurate and up to date.